Your Lifetime Effective Tax Rate

Ignoring your lifetime effective tax rate can be one of the more costly (and under discussed) mistakes investors make. Instead of optimizing for the following April, one should think bigger. Like decades bigger.

Lifetime effective tax rate can be defined as total tax paid divided by total income earned, both in life, and in death (we won't get into estate taxes here.) If someone earned $3m over a 40-year working career, and $500k of federal income tax paid on those earnings, they came out at a ~16% ($500k/$3m) effective federal tax rate.

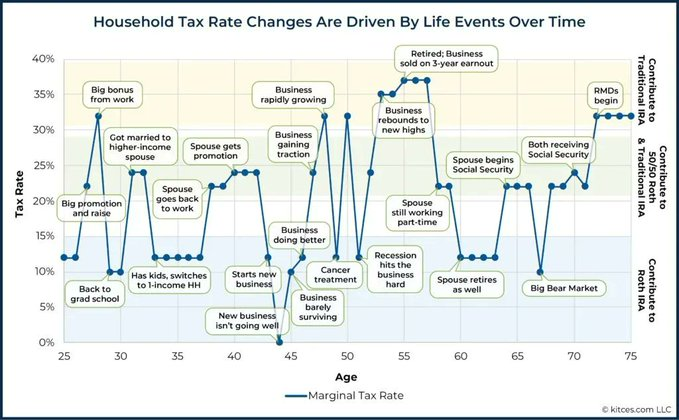

As it relates to income, there are seasons of life. Income tax is paid over the course of a lifetime, yet the highest earning years can be concentrated over a much smaller period of time. The chart below from Michael Kitces illustrates how tax rates are driven by life events. Rather than succumb to the peaks and valleys, there can be thoughtful planning that smooths out the ride to achieve a lower lifetime effective tax rate.

Let's walk through a typical timeline.

In your 20's, don't avoid tax, pay it. Maximize the Roth retirement plan. Start the process of saving in a taxable brokerage account. Buy your first rental property. Take full advantage of the fact that this is the lowest amount if income you're going to make, ever.

Ten years goes by in the blink of an eye, and you start earning significantly more income. Now would be the time to start using deductions to your advantage, perhaps in the form of pre-tax retirement plan contributions or a donor advised fund. These types of deductions remain valuable as long as income is high.

When transitioning to pre-retirement and the early retirement years, there can be a temporary window of opportunity that goes away once Required Minimum Distributions (RMD's) start (in the age 73-75 window, depending on your date of birth.) You may consider Roth conversions to take advantage of low rates or step up cost basis and create capital gains at 0%. You may also consider accelerating distributions from pre-tax retirement plans. The timing of layering in Social Security benefits is also a huge factor. Wasting these years is expensive, and most aren't even aware of it. This is an area of planning with clients where we spend a significant amount of time.

The same tax code applies to everyone, yet some are better using it to their advantage than others. Despite not knowing what future tax laws look like, or how your career may unfold a decade from now, there is still planning that can be done with the end in mind. Think in decades, not in years.

--

The content in this article was prepared by the article’s author and is not intended to provide specific advice or recommendations for any individual. Voya Financial Advisors does not endorse its content, and the views expressed may not necessarily reflect those held by Voya Financial Advisors.

Neither Voya Financial Advisors nor its representatives offer tax or legal advice. Please consult with your tax and legal advisors regarding your individual situation.