The Real Risk to Retirees

The prospect of a stock market crash stokes most of the anxiety for retirees. But inflation is the silent killer.

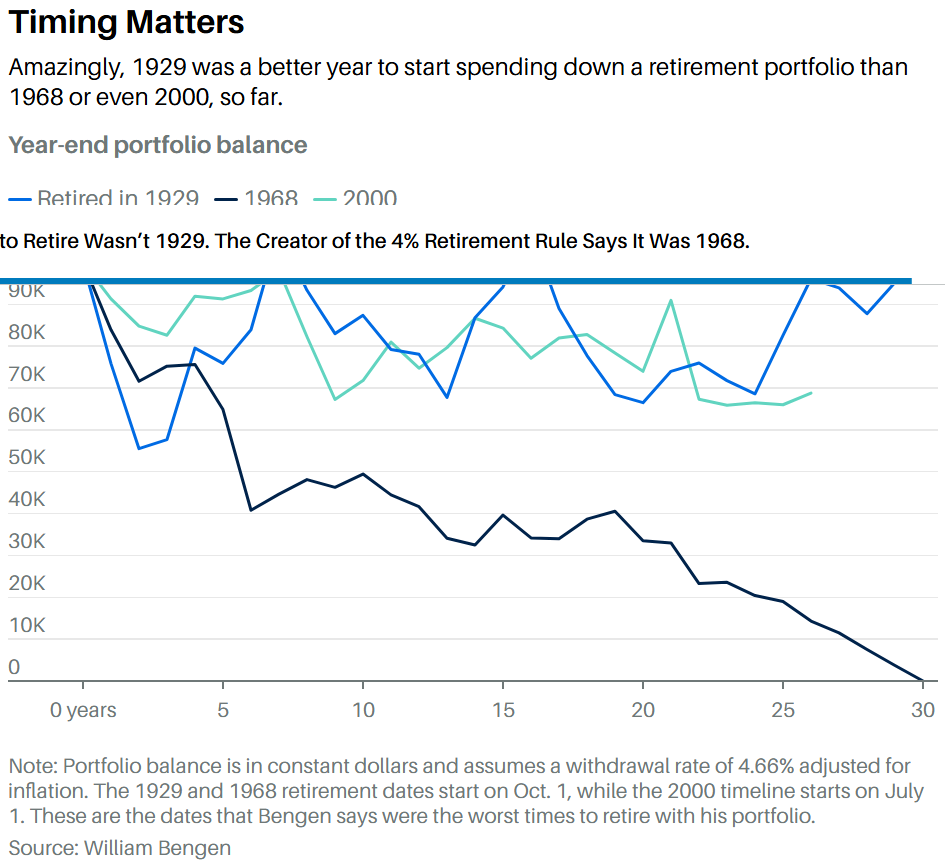

While timing of portfolio returns and sequence of return risk play into the calculation, they pale in comparison to persistent higher than anticipated spending needs. William Bengen, who coined the 4% rule, said it wasn't 1929 that was the worst time to retire. It was 1968. And the results weren't particularly close. From Barron's:

"Bengen found that if the 1968 retiree withdrew 4.66% annually, the account would be spent to zero in 30 years. By contrast, if the 1929 retiree took out this same percentage, he or she would have had a $105,000 account balance in inflation-adjusted dollars after the final withdrawal.

Put another way, despite retirement on the brink of the worst market crash of the 20th century and 30 years of withdrawals, the ending portfolio was actually 5% higher in constant dollars than the beginning portfolio. “Amazing,” Bengen says. “It was a heck of a recovery.”

Now compare that with the retiree unfortunate enough to stop working in October 1968 and start spending down his or her nest egg when markets were also in a funk. The $100,000 portfolio dropped sharply in the early years and never recovered. In six years, it was worth less than $41,000."

Do elevated stock prices cause concern that future returns will be more muted? Certainly. But inflation is the real risk to a retiree spending down their portfolio. And one that there doesn't seem to be a great strategy to combat.

--

Source: The Worst Year to Retire Wasn’t 1929. The Creator of the 4% Retirement Rule Says It Was 1968 Neal Templin (Barron's)